There are no items in your cart

Add More

Add More

| Item Details | Price | ||

|---|---|---|---|

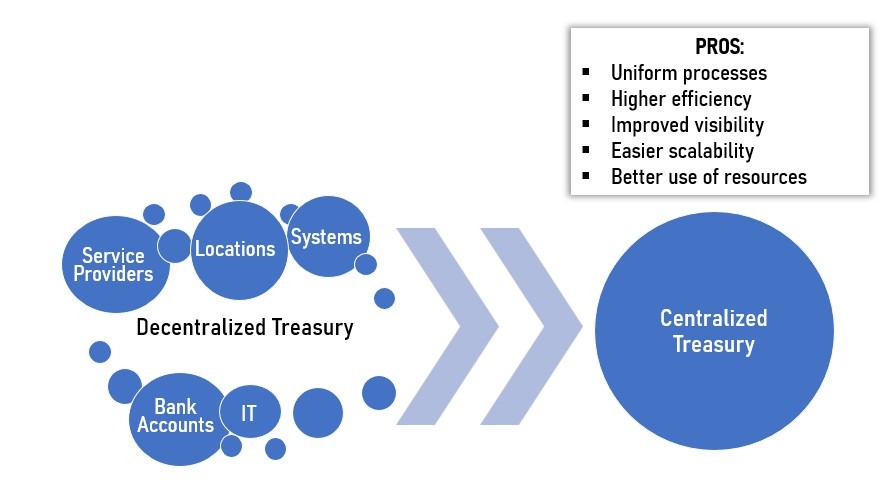

Most companies at the nascent stage, having presence in just a few countries, start with a decentralized model of treasury. In this model, each region or country office has its own regional treasury which manages almost all treasury tasks independently. So, each regional treasury will perform reporting, forecasting, risk management, collections, payments, reconciliation, invoicing and all other associated tasks for its own country or region. The treasury at the head office will only consolidate all numbers and frame the overall policy.

The advantage of a decentralized treasury model is increased flexibility and speed of operations where any decision can be readily taken by the local team itself. But a decentralized treasury results in an unstructured process which works without any uniformity as the control of the treasury is with the local management and each regional treasury may work in a different approach compared to the other.

As companies expand their presence in more and more countries, the complexities of treasury operation increases. In such cases a global company may decide to gradually move to more centralized models of treasury.

Various aspects of treasury like locations, bank accounts, cash management, service providers, systems and IT can be centralized to one or more locations. This can result in more uniform processes, higher efficiency, improved visibility, easier scalability, better use of resources and obviously more control at a reduced cost. This being said, the initial set up of a centralized treasury moving from a decentralized one can be challenging in both cost and operational aspects, and thus, most companies gradually move to a centralized model after a cost to benefit analysis.

Let us now see the varied degrees of centralization possible in a global corporate treasury.

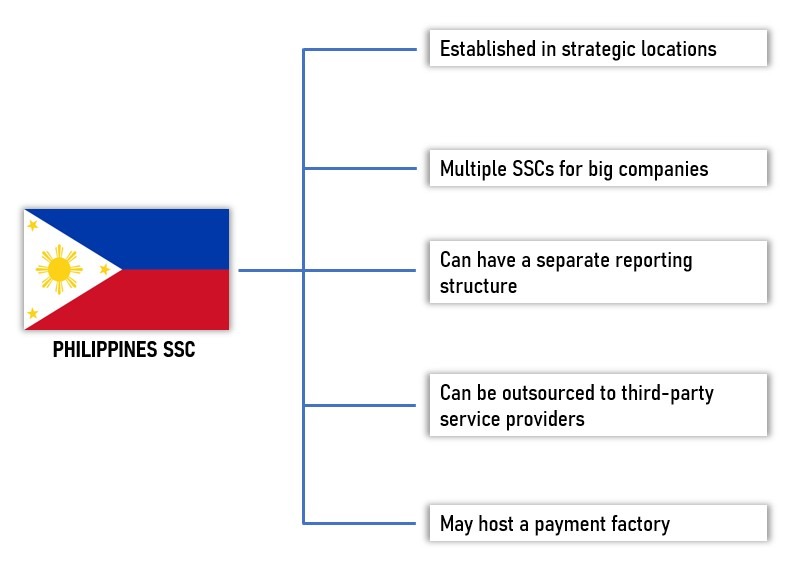

In a Shared Service Center model, the high volume and low complexity tasks of a treasury are moved to a separate center called the shared service center. An SSC usually handles accounts receivable (AR), accounts payable (AP) management, report generation, ledger entries etc.

The location of the SSC can be anywhere but choosing the location depends on various factors. An SSC is usually established in countries where labour and office cost is low. Also, countries which provide attractive tax structure with good infrastructure are chosen locations of establishing an SSC. For very big companies there can be multiple SSCs handling separate tasks for the entire company group. An in-house SSC can have a separate reporting structure and hierarchy handling large volumes of repetitive tasks. Smaller companies can even outsource their SSC to third party service providers to save expenses and human resources. An SSC may host a payment factory which handles centralized payment and collections for a company.

In a decentralized model, if an invoice is raised by a supplier, that is entered in the ERP system by the local office, it sits in the system till the due date of payment comes, on the due date a payment is initiated by the local office through a regional bank. In case of an SSC model, as soon as the invoice is raised by the supplier, it is sent to the SSC. In the SSC all such invoices are centrally recorded, managed and batch wise payment released according to due dates. Such transactions are called on-behalf-of (OBO) transactions, i.e. OBO payment where the SSC is making payment on behalf of some other subsidiary, and OBO collection when the SSC is collecting the payment due to some other subsidiary on its behalf. Using such a model the entire process becomes efficient and cost effective.

But OBO requires clear legal mandates, bank instructions, signatory controls and authorization frameworks to avoid operational and legal risk. Lastly, using SSC, trade finance and factoring facilities can be obtained by the corporate in a streamlined way.

Some companies create a global business services (GBS) group — also known as centers of excellence — to offer support to multiple business units. Unlike SSCs, GBS groups not only provide various services but also include business advisory functions, such as continuous improvement or internal consulting, to enhance operational efficiency across business units.

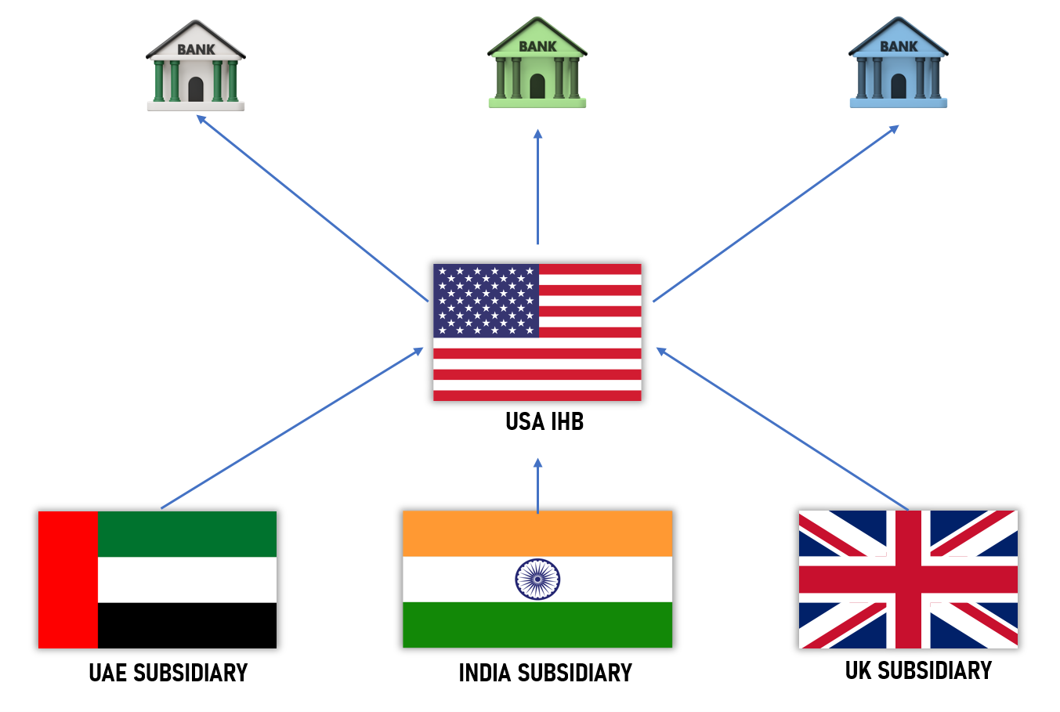

The most advanced stage of centralization of a global corporate treasury is the in-house bank model. In this model, the treasury is almost fully centralized and acts as a bank for all the offices and subsidiaries of the company. All account management, foreign exchange exposures, funding, funds transfer, invoicing or re-invoicing, investments, and risk management are done by the in-house bank for all the offices and the in-house bank in turn interacts with actual external banks for all these financial purposes by consolidating all the requirements. This results in better overall control, efficient cash management, better cash visibility, less requirement of external funding, competitive borrowing rates for the global company.

But this also requires lot of investment and maintenance cost and is usually justifiable for really large size global corporates. Also, though an IHB can operate like an internal bank for the group, its permitted activities, legal form and documentation depend on jurisdictional rules — in some cases regulatory/licensing or capital requirements and tax/transfer-pricing implications must be addressed.

WANT TO READ MORE?

Already signed up/ logged in? Then you are all set!

Basics of Payments | SWIFT MT/ MX Payment Message Types with examples | SWIFT GPI

Trade Finance Overview | Letter of Credit | Bank Guarantees and Standby | Incoterms® 2020

The Ultimate No-Nonsense Guide to SWIFT MT and ISO 20022 MX Message Types

Launch your Graphy

Launch your Graphy