There are no items in your cart

Add More

Add More

| Item Details | Price | ||

|---|---|---|---|

Multi-Currency Notional Pooling is a sophisticated cash management structure in a centralized treasury model that allows a company to offset balances in different currencies (e.g., USD, EUR, GBP) to calculate a net interest position without physically converting the currency.

It allows a global corporate treasury to use a surplus in the USA to offset a deficit in France or the UK, without paying foreign exchange (FX) transaction costs.

Let’s understand with an example.

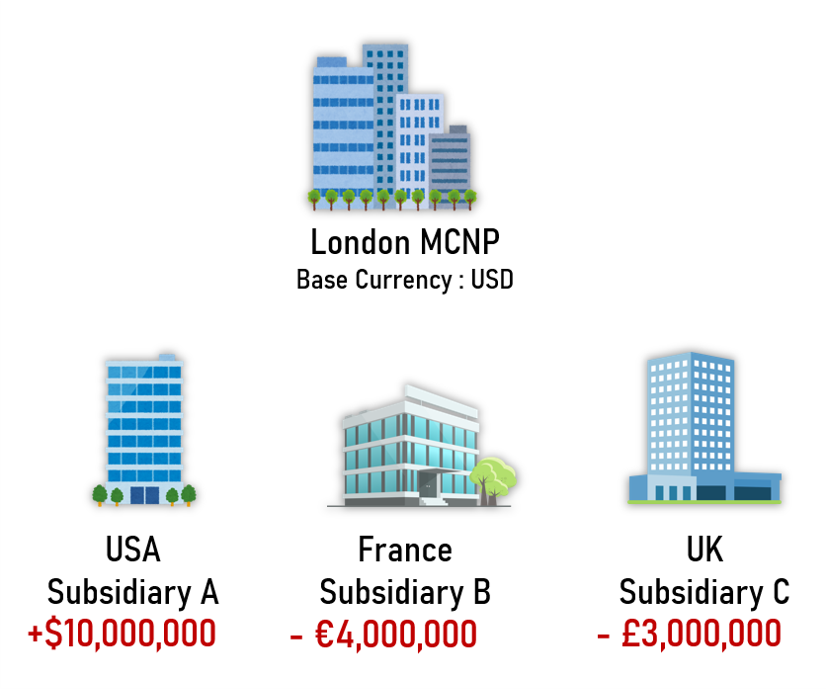

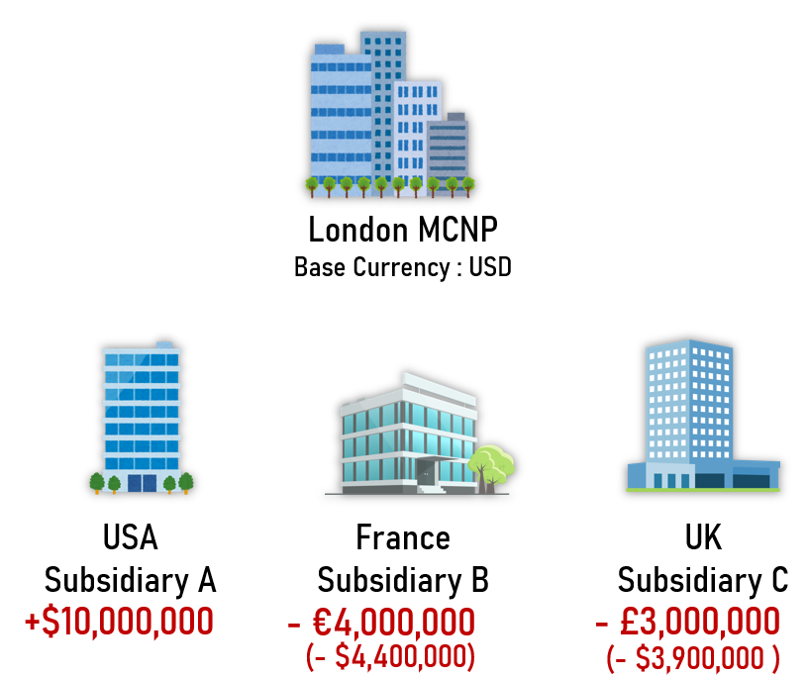

Let's assume Global Parent Co. sets up a Multi-Currency Notional Pool in London which is usually a common hub for this because it is a leading global financial and foreign exchange (FX) trading center. The "Base Currency" of the pool is USD.

Let us assume that €1 = $1.10; £1 = $1.30

Now let's see how MCNP works.

No Physical Movement: There is no physical movement of cash. Sub A keeps its USD, Sub B keeps its EUR, and Sub C keeps its GBP. No actual currency trading takes place.

Hypothetical Conversion: The bank virtually converts the balances of Sub B and Sub C into the Base Currency (USD) using a reference rate. So, Sub B has a deficit of 4M Euro which when converted to USD at the rate of 1 EUR = $1.10 USD, comes to $4.4 M. Similarly, Sub C which has a deficit of 3M GBP, when converted, has a deficit of 3.9M USD.

Sub B (France): €4M × 1.10 = $4,400,000 (Deficit)

Sub C (UK): £3M × 1.30 = $3,900,000 (Deficit)

Net Aggregation: Next, the bank sums up the virtual USD equivalents.

So, +10.0M(A)−4.4M(B)−3.9M(C)=+$1,700,000 Net Position

Now let's assume that:

The Deposit or Earnings Rate is: 2%

The Overdraft or Borrowing Rate is: 8%

Let's see what happens without pooling-

The Sub A in USA earns at the rate of 2% on $10M which comes to +$200,000.

The Sub B in France pays at the rate of 8% on equivalent dollars of $4.4M which comes to -$352,000.

The Sub C in the UK pays again at the 8% on equivalent dollars of $3.9M which comes to -$312,000.

So, the net result is that the group pays a net cost of $464,000.

In this case, the bank looks at the Net Position of +1.7M USD of the group. Hence the group earns at the rate of 2% on 1.7M USD which comes to $34,000.

Group: Earns 2% on $1.7M = +$34,000

Net Result: The group earns $34,000.

Total Benefit: Thus, the shift from a $464k cost to a $34k gain saves the company nearly $500,000 annually, simply by leveraging the USD surplus against EUR and GBP debts.

No FX Spread Costs: The primary advantage is there is no daily FX spread cost. If you physically swept the money, you would have to sell USD and buy EUR or GBP every day. The bank would charge a "spread" or fee on every trade. MCNP avoids this daily trading entirely.

Preserves Local Liquidity: Sub B in France still has its overdraft facility available in EUR. It doesn't have to worry about the Parent sending USD that it can't use locally to pay French taxes or suppliers.

Hedge Savings: MCNP acts as a "natural hedge." You are offsetting your long positions i.e., assets, against your short positions i.e., liabilities across currencies without using derivatives.

Basel III / Regulatory Capital: The biggest hurdle of MCNP is the Basel III regulations. Under Basel III regulations, banks cannot easily net these different currencies on their balance sheet.

Why? Because if the exchange rate moves wildly overnight (e.g., GBP crashes), the USD surplus might no longer cover the GBP deficit.

As a result, banks must hold capital against the gross overdrafts (i.e., the deficits of B and C) rather than the net. Consequently, banks often charge very high fees for MCNP to cover their capital costs.

Notional "Haircuts": To protect against currency fluctuation, the bank will not give you 100% value of your foreign currency.

For Example: If Sub A has $10M, the bank might only allow $9.5M of it to offset the EUR/GBP debts. Thus, the remaining un-offset debt pays high interest.

Limited Jurisdiction: Very few countries allow MCNP. It is typically only available in global financial hubs like London, Amsterdam, Singapore, or Hong Kong. You cannot easily set this up in Brazil or China.

Despite the high bank fees and regulatory issues, MCNP is still practical for:

Companies with High Volatility: If your subsidiaries have balances that swing from positive to negative daily, physical FX conversion is too expensive. In such cases MCNP smooths this out.

Exotic Currencies: If you operate in currencies with very high "spreads" i.e., cost of trading, avoiding the physical trade is worth the high monthly bank fee.

Short-Term Imbalances: It is excellent for managing short-term mismatches (e.g., you are excess in USD today but will owe USD next week, while being short EUR today).

WANT TO READ MORE?

Already signed up/ logged in? Then you are all set!

Basics of Payments | SWIFT MT/ MX Payment Message Types with examples | SWIFT GPI

Trade Finance Overview | Letter of Credit | Bank Guarantees and Standby | Incoterms® 2020

The Ultimate No-Nonsense Guide to SWIFT MT and ISO 20022 MX Message Types

Launch your Graphy

Launch your Graphy